Sometimes you just have to be forceful with dithering clients

/4 Ponderosa Drive, Cos Cob, $1.9 million, under contract after being listed just 16 days agao.

Greenwich, Connecticut real estate, politics, and more.

Greenwich, Connecticut real estate, politics, and more

4 Ponderosa Drive, Cos Cob, $1.9 million, under contract after being listed just 16 days agao.

13 Spezzano Drive, NoPo, $1.150 million, $1.250 million asked. Stamford buyer

48 Meyer Place, Riverside-I95, $1.479 million, original price $1.650. Greenwich (06830 Zip)

Meyer Place

30 Crescent Road, $4,137,500 paid on asking price of $3.850. West Village buyers (10014 Zip)

Crescent

Single-Family Home Sales

There were 59 single-family residential closings reported across all areas of Greenwich during the month of June 2025. This figure decreased, compared to June 2024 when there were 63 closings.

The Median Sale Price for a single-family home increased 56% to $3,900,000 from the median sales price in June 2024, which was $2,500,000.

The average Days On Market (DOM) for residential homes was 48 days; which was a 14.29% increase from 42 days in June 2024.

There were 58 new single-family listings brought to the market in May 2025, which is a 12.12% decrease in New Listings when compared to June 2024 when there were 66.

At month-end, Active single-family inventory totaled 141 units, which is a 28.8% decrease from June 2024 when there were 198 units available.

Condominium and Co-op Home Sales

There were 14 condo/co-op residential closings reported across all areas of Greenwich during the month of June 2025. This was a decrease, compared to June 2024 when there were 18 closings.

The Median Sale Price for a condo/co-op decreased 28.57% to $787,500 from the median sales price in June 2024, which was $1,102,440.

The average Days On Market (DOM) for condo/co-op residential homes was 39, which was a 7.14% decrease from 42 days in June 2024.

There were 18 new condo/co-op units brought to the market in June 2025, which is an increase of 20%, compared to June 2024 when there were 15.

At month-end, Active condo/co-op inventory totaled 33 units, which is a 5.7% decrease from June 2024 when there were 35 units available.

For the latest data and detailed breakdowns, click here to view the full market statistics reports.

Second Quarter Greenwich Market Update 2025

July 2, 2025 (Greenwich, CT) -

Single-Family Home Sales

There were 158 single-family residential closings reported during this period according to figures provided by The Greenwich Multiple Listing Service, Inc., the multiple listing service used by REALTORS® in the Greenwich area.

The number of single-family residential closings increased compared to Q2 2024 when there were 149 closings.

The median sale price for a single-family home increased to $3,175,000 from the median sales price in Q2 2024, which was $2,620,000.

The average days on the market (DOM) for residential homes was 54 days; which was a decrease from 58 days in Q2 2024.

Condominium and Co-op Home Sales

There were 46 condo/co-op residential closings reported during this time period; which was a decrease from Q2 2024 when there were 57 closings.

The median sale price for a condo/co-op decreased to $895,000 from the median sales price in Q2 2024, which was $1,144,880.

The average days on the market (DOM) for condo/co-op residential homes was 45; which was a decrease from 57 days in Q2 2024.

UPDATE: Well, damn — this didn’t actually happen. It’s still hilarious, but ….

You’ll never guess what happens next

From the Wall Street Journal

Surging defaults on loans used to buy residential solar panels are cascading through Wall Street, catching bond investors and private-credit funds in their wake.

About 50,000 U.S. homes had solar panels installed last year, up from about 14,000 in 2019, according to the Solar Energy Industries Association. Falling panel prices fueled the surge, but so did easy credit. GoodLeap and competitors like Sunnova Energy International and Mosaic funneled loans to homeowners through local dealers who sold panels door-to-door.

Glahn: “:Key takeaway: don’t buy anything sold door-to-door.

“You can read the WSJ story, but it all devolves into the ago-old story of asset-backed securities. If you’ve seen the movie Margin Call, you know how that ends.” [FWIW: The film details the massive fraud worked by Goldman Sachs, but of course, Goldman wasn’t the only bank involved in the scam, far from it — just ask Dickie Fuld, or any of his spiritual advisors and models at Enron.]

FWIW: I’ll excerpt a bit more of the WSJ article:

…. GoodLeap doesn’t keep any of the loans it makes, acting instead as a middleman that profits off fees charged for making and servicing the loans. The company is profitable and has pivoted to lending for home improvements such as heat pumps and energy-efficient windows, a GoodLeap spokesman said. The strategy helped GoodLeap avoid bankruptcy, unlike competitors who remained focused on solar. Most GoodLeap solar bonds still pay interest and are valued at 90 cents or more.

The firm finances the loans with borrowed cash, then quickly repays its debts by selling the loans to banks and private-credit firms such as Blackstone. Many buyers of the loans—though not Blackstone—paid for them with money raised by bundling them together into “asset-backed securities,” or ABS. Those are bonds guaranteed by the future payments the homeowners make on the loans. That strategy boosts returns if homeowners pay on time and worsens losses if they don’t.

The financing machine kicked into high gear when interest rates fell during the pandemic, and GoodLeap attracted tech investors such as Michael Dell, who valued its business at $12 billion. Banks such as Goldman Sachs, Citigroup and Credit Suisse sold $5.7 billion of GoodLeap solar bonds to investors, according to ABS data provider Finsight.

Credit-rating companies Fitch Ratings and KBRA gave most of the bonds investment-grade ratings based on analysis of similar deals backed by other consumer debt. When interest rates jumped in 2022, so did the cost of the solar loans.

[Remind you of the mortgage-backed securities peddled by Wall Street until 2008?]

Goldman sold $2.25 million of bonds backed by GoodLeap loans to an investment firm called the Catholic Responsible Investment Funds for nearly 100 cents on the dollar in 2022, according to analysis by The Wall Street Journal of data from Empirasign Strategies. Cumulative losses on the bonds rose to 3.65% in 2024, then nearly doubled this year to 6.3%, one of the people familiar with the matter said.

Traders recently quoted the bonds at 42 cents, according to Empirasign. A spokeswoman for Catholic Responsible Investment declined to comment.

“It was a brand new product…and people made good faith estimations, I suppose [“good faith, I suppose” — uh huh] of what default curves would look like and they happened to be worse,” said GoodLeap Chief Financial Officer John Shrewsberry.

Like other asset-backed securities, solar bonds are split into levels, or tranches, made up of pools of thousands of loans. Investors in the highest tranches get priority on payments and if defaults climb above preset thresholds, interest payments to the junior tranches stop.

Several bonds were close to breaching their thresholds earlier this year, but GoodLeap repurchased defaulted loans from the pools, preventing their triggers. By June, four bonds had defaults in excess of their thresholds, including the one owned by Catholic Responsible Investment. With no further buybacks, the interest payments halted.

14 Edgewater Drive, listed in June for $2.699 million, closed today at $3,304,000. Not bad for a house that sold for just $2 million in 2022. 1916 cottage of 2,686 sq. ft., renovated in 2013.

88 Cedar Cliff Road in Riverside, current price $13.995 million, has found a buyer and its sale is pending. The 1928 version of this home was purchased by these owners in 2008 for $11.750 million ($17,895,000 current dollars) and completely rebuilt and expanded beautifully and expensively. It was put back on the market in April 2022 for $25.5 million, and there it has sat for 1,162 days, slowly dropping its price. It long since fell past what I would thought was a fair value, and it’s been a streaming bargain for at least the past year. Someone finally noticed.

(Readers have asked about this before, so I’ll repeat: the land between this property and the shore was carved out and donated by the previous owners and deeded to the Land Trust in perpetuity, so the view and the use of that land is protected, with no tax due. An excellent proposition).

11 Roberta Lane Asked $2.250 million in December, accepted $1.9 in May. One-acre in the RA-1 zone, desirable street: Gentlemen, start your bulldozers.

just don’t kick me

Will anyone notice?* Any price cut in this development, these days, is unusual, but 28 North Ridge Road has been on the market for a full 30 days now at $2.8 million, so dropping it to $2.6 makes sense.

Decent-lookinghouse and location, it’s probably modular-built (the 2-story foyer is a hallmark of that type of construction) but there’s nothing at all wrong with that. Building a house in a factory, in a weather-controlled environment using computer-guided machines can make more sense than having a drunk with a hangover and a skill saw trying the same feat in a sleet storm. Besides, except for Jaguars, which come out of the factory unfinished and already falling apart, when was the last time you saw anyone assembling a new car in a customer’s driveway?

*Okay, that’s a fairly obscure reference, I suppose. Look up Bishop Berkeley.

Sale:

55 Long Meadow Road, Riverside NoPo, full asking price of $1.895 million. It was on the market for 49 days before finding a buyer, and that’s a long time in this market — it didn’t used to be – so I thought it might go at a discount, but they got their price, and good for them.

It was probably the guest cottage in the backyard that made the difference.

Under Contract:

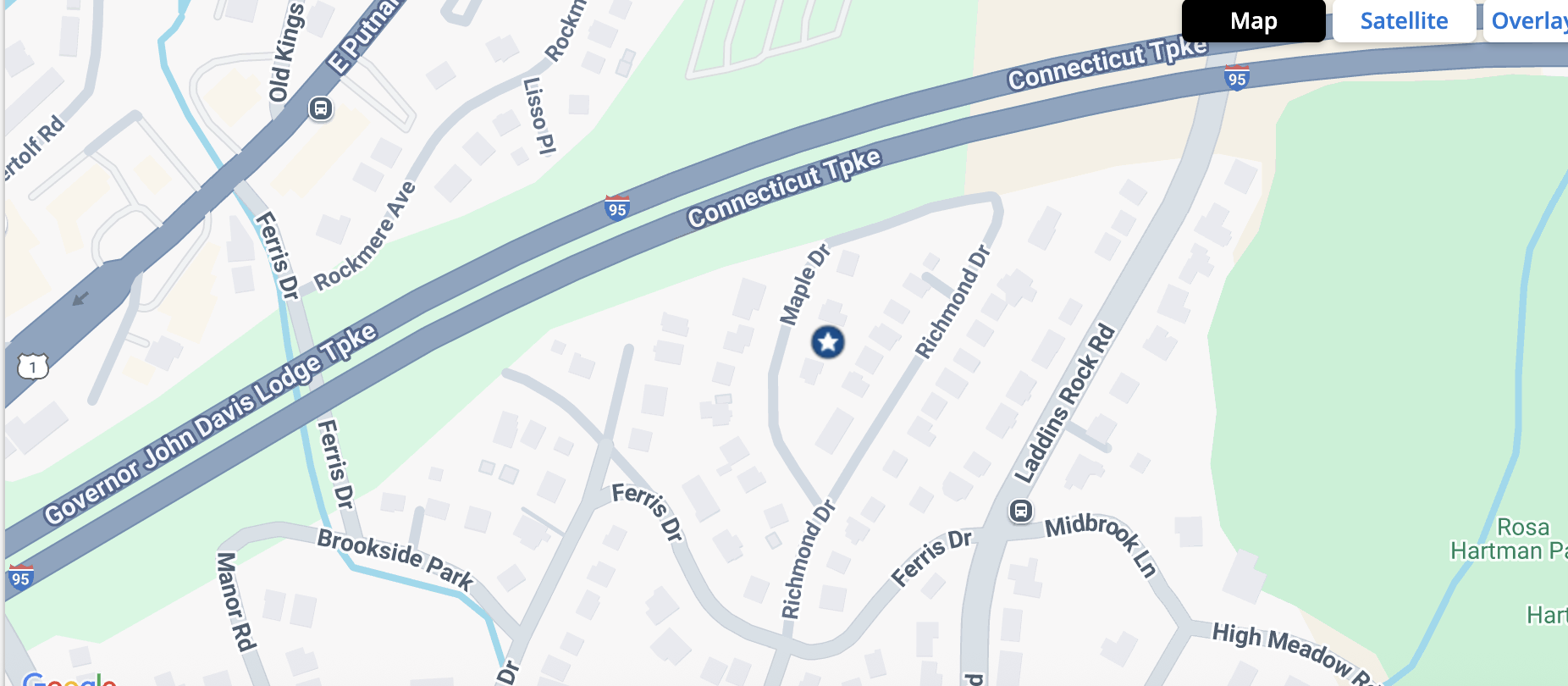

18 Maple Drive in Old Greenwich, 14 days on market. Asking price $849,000, it’s a 2-bedroom, 1 bath, 1,274 sq. ft. 1949 home on 0.10 of an acre. Smallsh for Greenwich, but it’s a perfect low maintenance down-sizer; heat it with a couple of incandescent light bulbs, cool it by propping an ice cube-filled wet towel in front of a window fan, and don’t worry about the lawn care workers’ sudden retreat to Mexico, you can trim this one with a pair of tweezers. Did I mention that it’s convenient to transportation? Well it is.

Be notified of new posts! Sign-up here:

Want to comment without registering?